NVIDIA’s Revenue Surge: A Double-Edged Sword?

NVIDIA’s Q2 2025 financial results showcase a company that continues to ride the wave of AI and data center demand, but they also raise questions about sustainability, market positioning, and strategic direction. While the numbers are undeniably impressive, a deeper look reveals several areas of concern and potential challenges that the company must navigate to maintain its dominant position.

1. Revenue Growth: Significantly surpassing market expectations

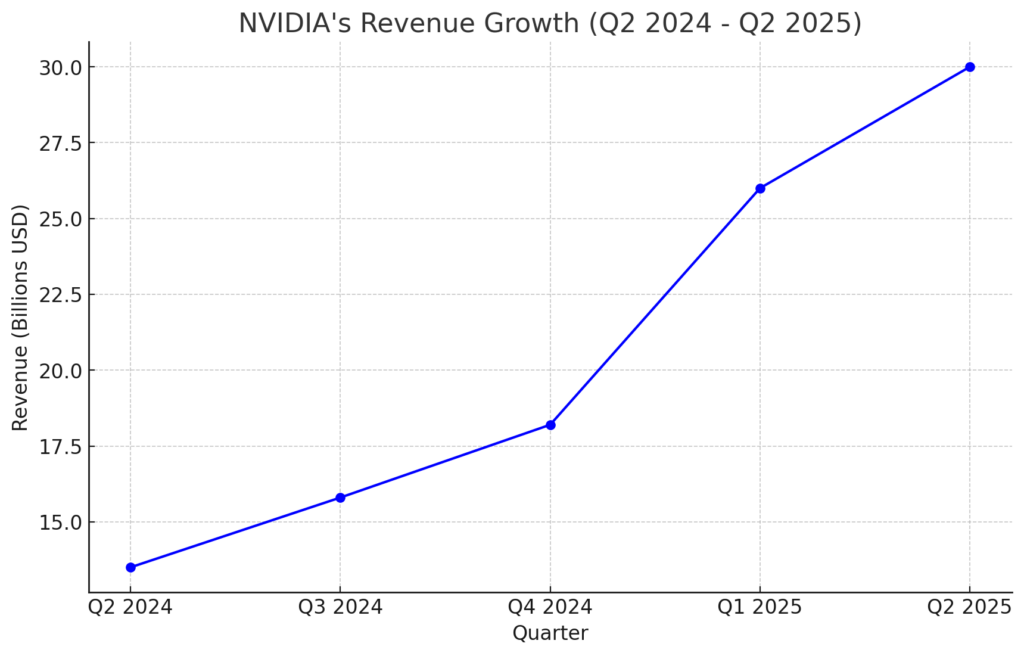

NVIDIA’s reported revenue of $30 billion for Q2 2025 represents a staggering 122% year-over-year increase. This growth is primarily attributed to the continued expansion of the AI and data center markets, where NVIDIA’s GPUs, such as the A100 and H100, remain the industry standard. However, this level of growth, while impressive, might not be sustainable in the long run.

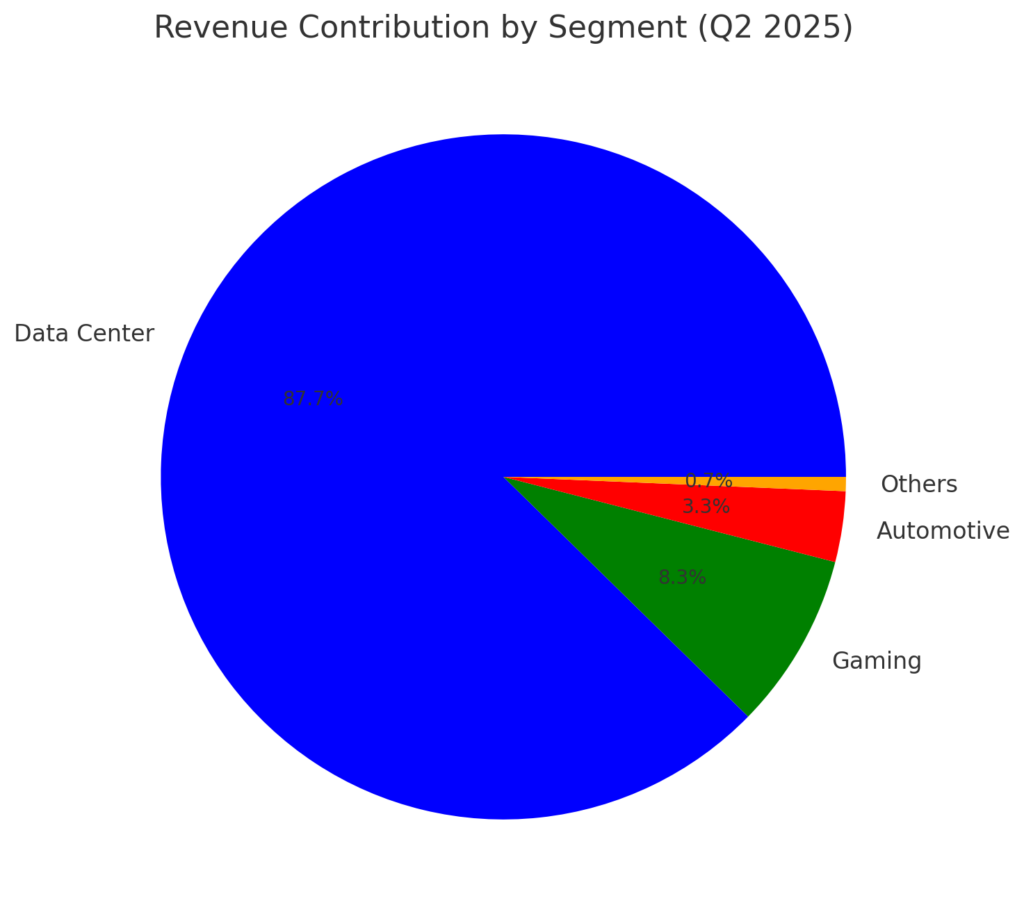

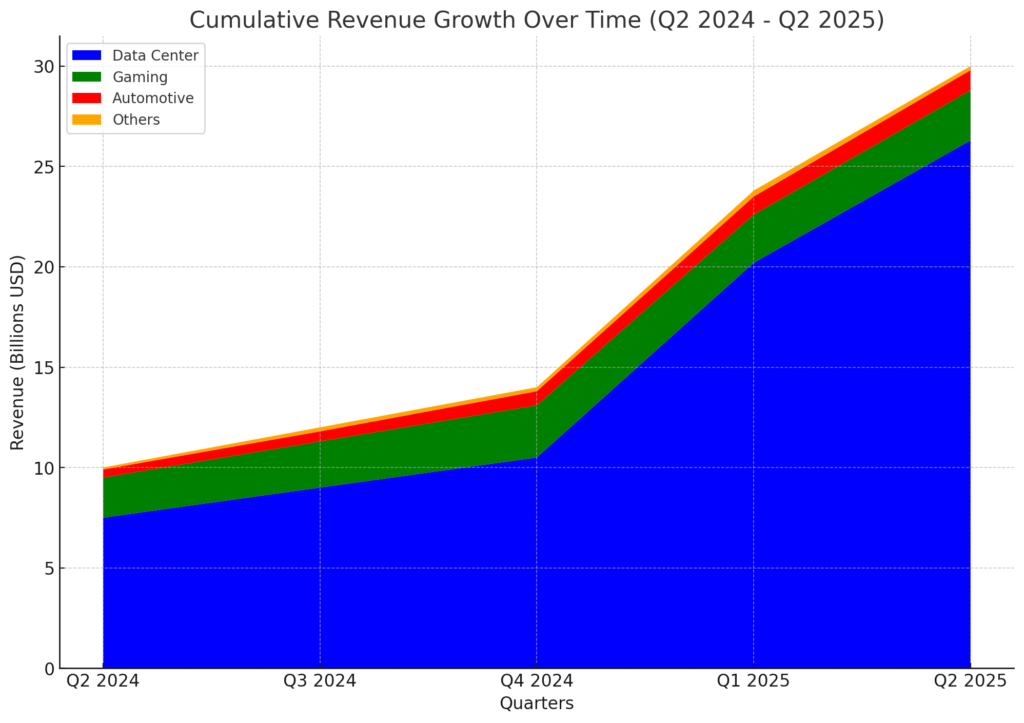

The company’s Data Center segment alone generated $26.3 billion, marking a 16% increase from the previous quarter and a 154% jump year-over-year. This growth reflects the continued investment in AI infrastructure by cloud service providers, enterprises, and research institutions.

The rapid adoption of AI technologies, while beneficial now, could lead to market saturation. If key sectors like cloud computing, autonomous vehicles, and data centers reach a plateau in their AI investments, NVIDIA might face difficulties maintaining this growth trajectory.

Additionally, while the company has diversified into gaming and automotive, these segments still pale in comparison to the overwhelming contribution from AI and data centers. This heavy reliance on one primary revenue stream makes NVIDIA vulnerable to shifts in market demand.

2. Gross Margin: A Sign of Market Pressure?

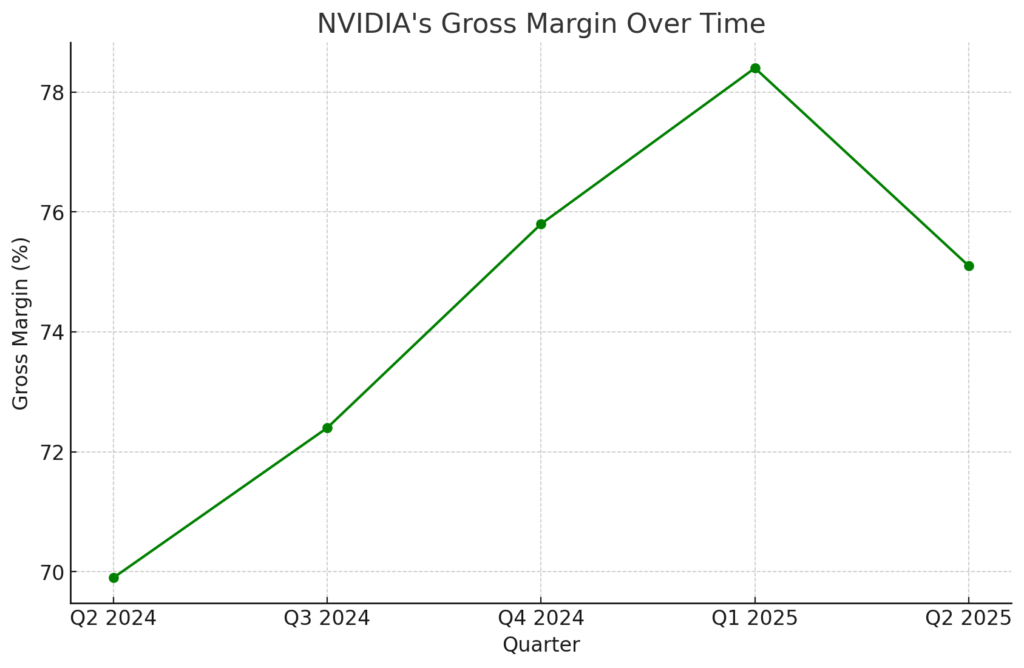

NVIDIA’s gross margin for Q2 2025 was 75.1%, a slight decline from the 78.4% reported in the previous quarter. While still strong, this drop could be indicative of several factors:

- Increased Competition: The decline in gross margin could signal increased competition from companies like AMD, Intel, and other emerging players in the AI chip market. As these competitors close the gap in technology and pricing, NVIDIA may be forced to lower its prices to maintain market share, which could further erode margins.

- Rising Production Costs: The semiconductor industry has been plagued by supply chain disruptions and rising material costs. If NVIDIA is facing higher costs to produce its GPUs, this could explain the narrowing margin. While NVIDIA has thus far managed to pass some of these costs onto consumers, the margin decline suggests that this strategy has its limits.

NVIDIA’s operating income for Q2 2025 was $18.6 billion, translating to an operating margin of 62%. Net income soared to $16.6 billion, up from $6.2 billion in Q2 2024, reflecting a sharp increase in profitability due to economies of scale and strategic pricing.

3. Profitability vs. Investment: Balancing Growth with Future Needs

NVIDIA’s operating income and net income surged significantly, reflecting the company’s ability to capitalize on current market opportunities. However, as NVIDIA continues to invest heavily in AI supercomputing infrastructure and partnerships (such as its collaboration with Google Cloud), there is a risk that these investments may not yield proportional returns in the short term.

The announcement of a $10 billion share buyback program signals confidence in future growth, but it also raises questions about whether these funds might be better allocated toward research and development (R&D) or strategic acquisitions that could ensure long-term competitive advantage. The challenge for NVIDIA will be to balance shareholder returns with the need to continue investing in innovation, especially as competitors intensify their efforts in AI and data centers.

4. Strategic Risks: Dependence on AI and Data Centers

While the AI and data center segments have been incredibly lucrative for NVIDIA, the company’s heavy reliance on these sectors poses strategic risks. The AI market is rapidly evolving, and while NVIDIA currently enjoys a dominant position, the competitive landscape is shifting. New entrants, advancements in alternative technologies (such as quantum computing), and potential regulatory hurdles could disrupt NVIDIA’s growth trajectory.

Moreover, as AI becomes more embedded in various industries, the demand for custom solutions could increase, which might not always align with NVIDIA’s current product offerings. Competitors that can offer more tailored solutions could start to erode NVIDIA’s market share.

5. Regulatory and Ethical Concerns

As NVIDIA continues to grow, it will likely attract increased scrutiny from regulators, particularly in areas related to AI ethics, data privacy, and antitrust concerns. The company’s global operations and dominance in key markets could make it a target for regulatory actions that could impact its profitability and operational flexibility.

Additionally, as AI technologies become more pervasive, there is growing public concern about the ethical implications of AI. NVIDIA’s role in developing the hardware that powers AI systems puts it at the center of this debate. The company will need to navigate these ethical challenges carefully, balancing innovation with responsible development.

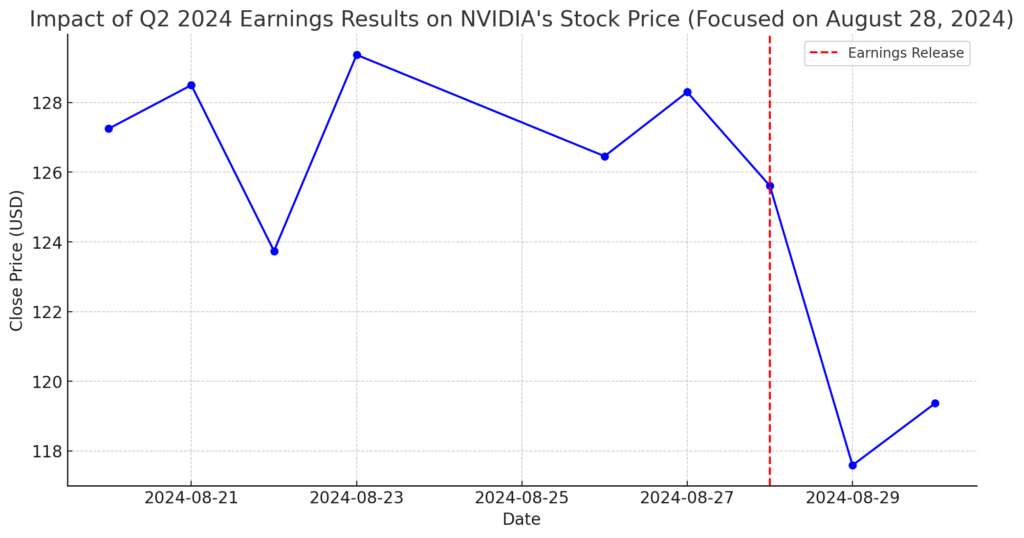

6. Stock Performance

Despite the strong financial results, NVIDIA’s stock experienced a decline of over 5% in the days following the earnings release. This drop reflects investor concerns about the sustainability of the company’s rapid growth, particularly in light of potential market saturation in AI and data centers. Additionally, the market may be factoring in broader economic uncertainties, such as inflation and interest rate hikes, which could impact tech stocks more broadly.

7. Market and Competitive Landscape

NVIDIA continues to dominate the AI and data center markets, but it faces increasing competition from companies like AMD, Intel, and new entrants in the AI chip space. The delay in the release of NVIDIA’s Blackwell AI chip series, combined with ongoing investigations by the US Department of Justice into potential anti-competitive practices, adds to the risks that could affect NVIDIA’s market position.

However, NVIDIA’s strategic partnerships with major tech companies, including Google, Microsoft, and Meta, provide a strong foundation for continued growth. These partnerships not only drive demand for NVIDIA’s products but also position the company as a key player in the AI ecosystem.

8. Media Reaction

In their coverage of NVIDIA’s earnings report, CNBC and Bloomberg highlighted the mixed market reaction despite the company surpassing revenue and EPS expectations. CNBC pointed out that while the financial performance was strong, investor concerns about the sustainability of NVIDIA’s growth and potential market saturation led to a sharp decline in stock price following the earnings announcement. Bloomberg echoed these sentiments, emphasizing that the market is increasingly wary of whether NVIDIA can maintain its rapid growth in the face of rising competition and broader economic uncertainties.